It’s difficult to provide an excellent customer experience when an employee is worried about whether he or she can afford a financial shock, such as an unexpected home repair or a medical emergency. For many customer-facing employees, one unexpected expense can quickly snowball into a larger problem: repossession, eviction, or other life-altering situations.

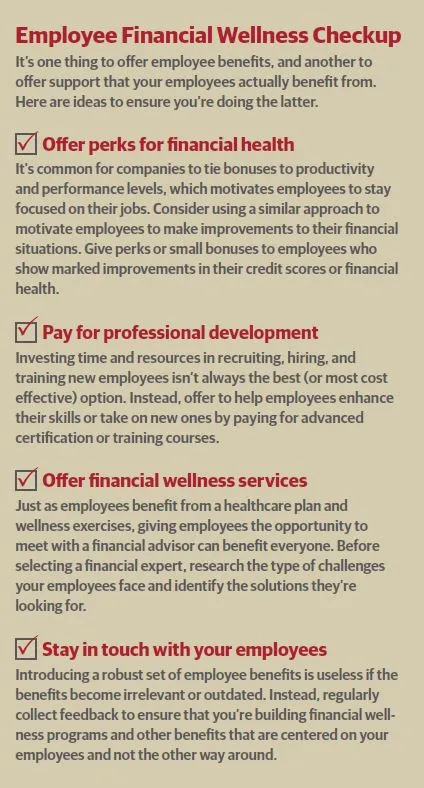

The financial well-being of a company’s employees has a significant effect on their performance, the customer experience, and ultimately the company’s bottom line. Simply raising wages isn’t always an option, though, which is why employers are turning to other ways of helping employees stay financially solvent.

Harvard improves EX with credit resources

Harvard University is one such organization that has drawn a connection between financial wellness and the employee experience. And while financial wellness programs are not new, the scope, objectives, and efficacy of the programs vary. Kerry Beirne, director of human resources for campus services at Harvard University (which includes dining, housing, buildings & facilities, and other services), says she was looking for a program that in addition to “just providing information, produced concrete results quickly.”

In 2015, Beirne learned about Working Credit, a nonprofit organization that helps employees build strong credit scores and reduce expenses that were inflated by poor credit or no credit. The program starts with a 45-minute workshop in which employees learn about how the credit system works, how a credit score is generated, what pushes the score up or down, how credit affects their daily finances, and how to build credit.

At the end of the presentation, attendees could sign up for individual financial counseling sessions. The counselor reviews the employee’s credit score and goals, and helps the employee create a personalized Credit Action Plan. The counselor then reviews the latest credit report and score with the employee every six months for 18 months and offers personalized advice. For example, if an employee had been paying inflated insurance premiums due to poor credit, once the employee reaches a threshold score, the counselor may advise the employee to negotiate a lower premium.

Having the opportunity to meet with a financial expert who can guide employees through the process of improving their credit score was an essential part of the program’s success, says Susan Simon, senior human resources consultant at Harvard University. “It’s not as if you hear something once and then forget about it. Working one-on-one with a counselor is incredibly valuable.”

The first time the program, Make Credit Work For You, was introduced to campus services employees, was in 2015. Of the 125 people who attended the workshop, 77 percent signed up for the counseling sessions. Results included a 39 percent increase in the number of employees with prime FICO scores (> 660). The number of employees with at least $1,000 available on credit cards also increased by 45 percent.

Recently, the university offered Working Credit’s program a second time, and “employees who had already participated, actually stood up and said the program helped them purchase homes and refinance their car,” Beirne says. “We didn’t expect people to share that, but it’s evidence this program works.”

In addition to partnering with Working Credit, the university has invited experts to share information about mortgages, retirement savings, and other topics that their employees may find useful. Speaking with employees and paying attention to their needs is key to understanding what employers can do to help, Simon says.

The impetus to introduce a financial wellness program like Working Credit’s, “didn’t come from a survey, but from conversations with some of our employees about their struggles as working mothers, difficulties getting to work, and other challenges,” Simon says.

Financial wellness pays off for employee engagement

Financial stress, which is sometimes due to a lack of financial literacy, affects people across industries at home and at their jobs. According to a study conducted by the Society for Human Resource Management (SHRM), 83 percent of HR professionals reported that personal financial challenges had a large impact or some impact on overall employee performance. On a similar note, almost half of employees who are worried about their financial health are less productive at work and spend at least three hours each week dealing with personal financial issues, according to a PwC report.

The impact of employee financial wellness on productivity and quality of work is obvious. Employers are taking notice. Last year, nearly 50 percent of employers offered financial advice in some form, according to SHRM, and that percentage is expected to continue to grow.

There’s a growing awareness of the connection between employee financial wellness and the customer experience. Wise employers understand that their job is to enable employees to be successful at their jobs, which includes helping employees be financially healthy. Creating an atmosphere that encourages financial well-being allows employees to perform to their full ability, which naturally benefits the business as well.