Walk into any bank’s headquarters and you will likely hear senior management discussing “multichannel strategy” or “omnichannel strategy.” They are ideas full of discussion, but still in the early stages of implementation. And while most banks look to non-branch channels for customer service, until now there has been limited exposure to omnichannel strategy in the sales and advisory domain.

To grow, banks need to expand their sales and advisory services into non-branch channels. Understanding and measuring the return on this investment will be the defining success factor for consumer banking institutions.

Multichannel versus omnichannel

Multichannel banking is about introducing new everyday channels and encouraging customers to use the most cost-effective ones. But, to accomplish this, channels and the complicated IT systems they required were bolted on to legacy systems and often operated in silos. Now, it is clear that siloed operations amidst a tangle of legacy systems is not the answer to retain and grow customers.

Omnichannel strategy takes the notion a step further to be customer-centric and provide consistent, seamless, and updated interactions across all channels. Customers decide the best channels to use, and any interaction should follow them as they move through channels. This differentiation can mean a lot of bottom-line impact: a recent Cisco study predicts that omnichannel solutions for banking are estimated to reduce customer revenue leakage by up to 70 percent and boost sales of complex products such as mortgages by up to 60 percent, while also significantly increasing employee productivity and customer satisfaction.

An omnichannel strategy involves integrating disparate systems, enhancing customer processes, and gaining a 360-degree understanding of each customer to align offerings to individual priorities. This means improving data integration and customer interactions as they move through sales channels. For example:

The branch: Many branches are integrating mobile, digital, and in-person capabilities in one physical space. Some branches are being re-imagined as a leading channel for sales and advice, staffed with sales-based employees with specialized training and high-value customer concierge services. And for good reason: A 2013 Cisco report found that 83 percent of consumers say they would be somewhat or highly interested in bank branches that offered an expanded portfolio of financial and advisory services including financial education, legal, accounting, tax, and insurance.

Branch managers are likely to make sales, coach employees, and be close to the business; and branch staff will evolve into ‘universal bankers’ who can perform all functions, for service, sales, or advisory. Relationship managers will move out of meeting in a branch to be more of a field sales force.

Contact center: While contact centers are still primarily service centers, they are growing as sales channels by leveraging data and integrating with other channels. For example, online video technology is increasingly used for advice, often hosted by dedicated relationship managers from branches or who have expertise in particular areas of need. Moving simple transactions and queries to the IVR and online will push the call center to be a sales- and advice-driven hub, which could convert upwards of 15 percent of service requests into sales.

Digital: The key to digital sales success will be complete origination and fulfillment outside the branch, even for complex products like loans. For example, Garanti bank in Turkey uses smart pens to activate accounts and fully acquire customers through the Internet and ATM.

To provide advice, leading banks are leveraging multiple avenues, such as online portals, professional research tools, automated product recommendations, comparison portals and online aggregators, as well as social networks. Video, chat, and instant messaging functions with staff members are also being leveraged for personalized advice. In addition, peer recommendations bolstered by crowdsourcing principles are also set to become a widely used and accepted method of general information sharing.

Designing bank digital channels to create a ‘wow’ experience for the user will ensure that customers’ digital tongues will wag. That’s why it’s so important to maintain a social media strategy and active, engaging presence online.

Omnichannel sales connects revenue to channel investment

Many omnichannel decisions require major investment, usually in new technology. However, costs can be offset by savings on legacy systems, lower distribution costs, and changes in the distribution mix that drive down operations and indirect costs. An assessment of European banks shows that such improvements may reduce costs by up to 40 percent. But senior leaders must understand the roles that different channels will contribute to the overall transformation—kneejerk reactions based on cost rarely lead to the best results.

Some banks look to fill the cost gap by adding fees for using different channels, but that inside-out thinking will result in customer avoidance. Instead, banks need to derive gained value by improving their channels through sales, cross-sell, and retention activities. This drives direct revenue by providing more sales touchpoints for the customer and more personalized and relevant sales offers for each customer in preferred channels. In addition, such initiatives improve the bank’s brand value and customer experience, which drives indirect revenue for the bank.

To get a clear idea of the return involved, banks need to assign costs and allocate cost-to-serve for each channel and/or sales and advisory interaction, and determine how those channels and interactions generate revenue. There is no ROI silver bullet, but evaluating customers’ purchasing behavior in an omnichannel world will help select the most appropriate calculation for the bank.

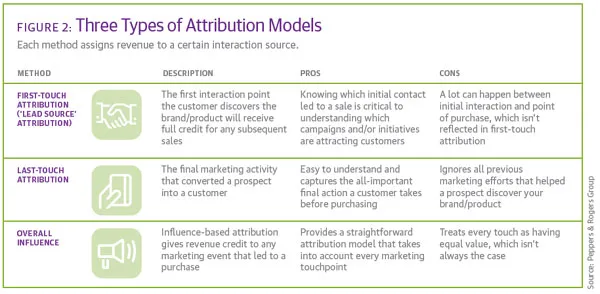

Attribution modeling is one method used to assign a revenue value to a purchase decision or sales channel. It is a technique used to effectively measure revenue from sales, especially in the digital realm. Figure 2 outlines three common attribution modeling methods used to measure this revenue gain.

Case in Point: SNS Bank

Recently, Forrester Research profiled omnichannel efforts of SNS Bank in the Netherlands. Its goal is to stand for simplicity in finance by “letting customers determine how, where, and when they take care of their financial affairs,” according to the bank’s website.

SNS reorganized branches into a network of lean, cashless, efficiency-oriented banking shops that served as a physical extension of the Web. Its new website provides extensive self-service functionality, and acts as an inbound marketing and sales channel. In addition, the bank added 150 new physical branches and introduced a mobile sales force that specializes in selling complex products. Finally, the bank extended its ATM network and reorganized the call center for inbound and outbound sales. It uses a centralized marketing platform that accesses historical customer records, interaction data, and Web clickstream data to create personalized inbound and outbound offers.

With the new strategy, SNS Bank assigned sales credit on a geographic level rather than at a channel level to increase the marketing effectiveness and ROI of the omnichannel environment.

As a result, the bank expects it will sell three times more products online in a three-year period, and twice as many complex financial products like mortgages and pension products. In addition, its Net Promoter Score jumped 34 points since 2010, and it reduced branch operating costs by 40 percent, leading to a cost/income ratio of 57 percent.

There are some clear best practices observed in SNS Bank’s omnichannel sales strategy:

Define a clear vision and stick to it: SNS Bank’s vision was developed four years before it came to life, but the vision still remains valid. By sticking to a clearly defined strategy, channel strategists at the bank knew exactly what they should do and not do.

Use carrots, not sticks to right-channel customers: Instead of just eliminating services from branches to migrate customers to digital channels, SNS Bank made sure that it could deliver the same or better service through self-service channels. Thanks to application pre-fill, for example, an application for a simple savings product can be done much faster online than it could previously be done in the branch.

Expect to take losses at first: SNS Bank’s customer satisfaction scores dropped when the new strategy was first implemented, but it is now picking up again. Strategic change often requires accepting losses in the short term.

Implement the strategy step-by-step: Instead of making major changes to all channels at once, SNS Bank took a step-by-step approach in implementing the strategy. It started with creating the website as the base, then focused on reorganizing the branch and mobile sales force. This approach helped the bank to keep a monumental project manageable.

Taking a dedicated and structured approach to transforming sales and advisory channels will ensure that banks continue to be relevant to the evolving consumer market and maintain their competitive advantage well into the future.