Digital technology is transforming every aspect of the property and casualty (P&C) insurance industry. Telematics, the sharing economy, big data, digital communications platforms, and an ever-changing competitive landscape have shifted the focus from products and process to a personalized customer experience.

Consumers are using insurance differently and have different expectations of their insurers than in the past. P&C firms need to be ready to respond with both technology and a comprehensive customer strategy when they interact with members.

It’s not an easy task. The “Amazon effect” means consumers expect the highest quality experience with every interaction from every industry. At the same time, people have different insurance needs than they used to. Young adults are waiting longer to buy homes and driving less. Members want more personalized products and services to match how they live, and are willing to turn to non-traditional brands to find them.

Technology and data insight also offer a great opportunity to personalize the experience around the customer instead of focusing solely on products. Telematics, mobile apps, self-service, drones, and other advancements are changing products, pricing, claims, services, and other aspects of the industry for the better. And investors are willing to cash in: the burgeoning “insurtech” industry has reached more than $1 billion in funding, according to CB Insights.

All of these trends spark opportunities for P&C insurers to get smarter about their approach to members and how they do business. There is enormous potential to reduce cost and risk while improving relationships.

We have identified four potential insurance technology trends for P&C executives as the customer experience, digital banking transformation, and technology intersect: next-gen product expansion, telematics, usage-based insurance, and chatbots.

1. Changing consumer needs open up a new universe of products

There are plenty of new products that were not even a twinkle in the insurance industry’s eye a decade ago. Identity theft protection, property insurance extensions, specialized car insurance for ride-sharing passengers, and self-service apps that remove layers of inefficiency are some new ideas being implemented or considered.

Many executives in the industry want to shed their laggard reputation, and it’s tempting to jump on the tech bandwagon. But without a burning platform from the customer perspective, it could be a wasted effort. Rethink products to meet actual customer needs, not just because it would be a cool way to use technology. In addition, leverage the immense data available to enhance existing products and services. Not everything has to be reimagined. A more personalized, relevant incremental change may be all that’s needed. Make yourself available in the channels your members will prefer. Mobile is gaining ground, for example, especially for members who think of products and services while on the go.

CX consideration:

Insight powers the connected home

The connected home consumer is motivated by convenience, peace of mind, and the potential to save money and resources. The benefits to insurers can be even more significant. Fueled by data, proactive and preemptive outreach to customers is just the tip of the iceberg. Strategic benefits such as new product offerings, a more robust supply chain, and more personal interactions offer top-line potential, as well. To realize these dual benefits, turn usage data into customer insights to more specifically uncover customer needs, engage them in the right channel at the right time, and personalize interactions throughout their journey.

2. Telematics offer personalization at scale

Telematics is the practice of taking diagnostic data directly from a device and sending it to your insurer. Telematics provides a direct source of customer insight that enables a range of digital insurance strategies and tactical opportunities to drive revenue, cut costs, and build deeper, more profitable relationships.

There is buzz growing around the technology’s potential, and adoption is slowly growing, with privacy a top concern. And our research shows that there is potential for companies to increase adoption and build competitive advantage by approaching the program with customer focus (see research sidebar).

Telematics encourage safe driving behavior that results in fewer accidents, helping insurers reduce claims payouts and improve the bottom line. According to a Cisco Internet Business Solutions Group report, vehicle connectivity can contribute up to 80 percent of savings in claims and cost containment. As insurers further analyze driving behavior, greater insights will emerge that will benefit underwriting and claims, as well as sales and retention.

Technologies such as advanced crash notification can provide first notice of loss for insurers to aid in response time and triage of claims, generating cost savings. With more accurate accident data available in real time, insurers can more accurately and efficiently settle claims, deliver fraud detection, and offer immediate assistance, such as emergency response, tow, rental cars, and repairs.

In the home, telematics can connect to in-home video cameras to perform digital inventories of the home’s contents, expediting claims filings and making it easier to remediate losses. And utility partnerships can help insurers analyze energy consumption data and usage activity patterns to increase the sophistication of pricing liability and/or dwelling coverage.

CX consideration:

The long tail

Telematics allows insurers to develop new auxiliary revenue channels, as car makers introduce add-on connected-car services that benefit consumers with a more frictionless experience. They include in-car entertainment, WiFi, real-time navigation, and emergency roadside assistance. Insurers offering additional value will also offset the initial costs of a usage-based insurance (UBI) initiative.

3. Usage-based insurancepricing gains ground

Insurance has traditionally been an industry all about aggregate data. Underwriting and risk assessments are calculated with broad demographic and geographic profile data. UBI turns that model upside down with the ability to set premiums and policies based on individual usage, propelled by telematics.

It’s a growing trend that has benefits for both P&C insurers and their members. Within three years, usage-based insurance policies are expected to account for 20 percent of all vehicles insured in the U.S., according to the National Association of Insurance Commissioners.

As insurers begin offering this option to members, notable customer experience opportunities emerge. For example, awareness of UBI has grown from 39 to 43 percent since 2015, but companies that exclusively market it as a way to save on premiums may exclude customers not motivated by discounts. In addition, among consumers who are offered UBI, half enroll—yet only one in five reports being offered UBI at all.

Also of note, consumers are waiting for unfettered feedback before signing up. According to a recent survey, 56 percent of respondents said they wouldn’t enroll in a UBI program until feedback or reviews are available, and 40 percent said they wouldn’t enroll unless someone they knew participated first.

And finally, UBI is typically thought of as a solution for younger members, and with good reason. Towers Watson reports that 72 percent of Millennials believe it is a good way to calculate auto insurance rates. However, there is also growing interest from consumers between the ages of 45 and 64.

CX considerations:

Look past discounts as a strategy

The insurance industry should adopt marketing and incentive strategies other than discounting to expand market share without sacrificing the bottom line, such as roadside assistance, improving young driver safety, or minimizing a driver’s carbon footprint. In addition, launch word of mouth, social media marketing, and customer testimonials to increase UBI adoption. Build advocacy among users by emphasizing the benefits that align best with the target audience by understanding customer value, needs, and wants.

4. The growth of P&C chatbots

Chatbots are on the rise, and the P&C market is just starting to understand how to best deploy this emerging technology. Chatbots are automated interactions done through popular messaging platforms like Facebook Messenger, WhatsApp, and other in-app chats. They even extend into conversational user interfaces like Alexa and Google Home. They combine chat technology with artificial intelligence and a dynamic knowledgebase to support automated conversations with real people. Business Insider reports that 60 percent of Gen-X and Millennials have interacted with a chatbot on a messaging app.

Insurance companies are learning how chatbots can improve sales and marketing, underwriting, claims, and customer service. For customers, the technology is used to demystify complex products, walk them through complicated service interactions and even guide users to the right policy. The complex and sometimes empathetic nature of many insurance interactions require companies to be prudent about automating with chatbots.

CX considerations:

Watch and learn

While it’s still early days for the industry, there is great potential to deliver a more personalized experience in the channel of the customer’s choice while tapping a data source to further understand user habits and personalize the customer experience. Track the pulse of your members’ preferences to determine if and where chatbots should be deployed for certain customer interactions.

These are some of the major technology trends being applied in the insurance industry. Matched with changing customer expectations, they reveal an industry being disrupted around great experiences and customer insight.

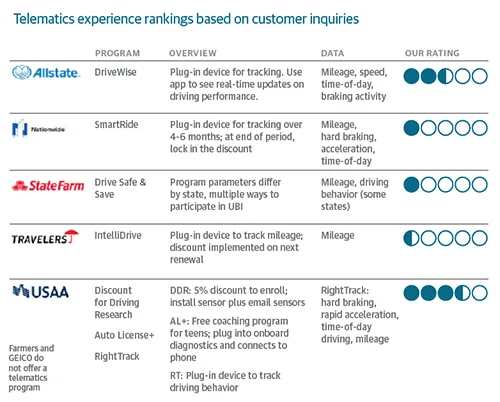

Research uncovers lost telematics opportunities

Usage-based insurance (UBI) programs that use telematics are seen as essential in the evolution of P&C insurance to be more personalized and cost effective. There are numerous benefits to consumers in the form of lower premiums and frictionless services, as well as to companies with more precise data and risk mitigation. Yet how effectively is UBI being communicated to new customers?

TeleTech researchers contacted seven leading companies in early 2017 to inquire about telematics services: Allstate, Farmers, Nationwide, GEICO, State Farm, Travelers, and USAA. They reached out via voice, chat, web self-service, social, and email. Inquiries were made across a range of issues to see whether UBI would be offered during the interaction. We then rated each company on a five-point scale according to channel availability, timeliness of the telematics offered, and value of information provided during the interaction. Here’s how they scored:

USAA scored highest on availability, timeliness, and value of telematics information to the consumer. The company did not proactively offer the tool, but was effective in responding to inquiries. Associates were well informed and particularly effective in talking through privacy concerns that our secret shopper analysts raised. Allstate operated similarly, though without as much robust associate knowledge.

Comparatively, Nationwide and State Farm presented telematics only as part of automated Get Quote website tools. Sales associates were not prepared to discuss the option. And Travelers associates answered questions about telematics on Facebook and Twitter, but nowhere else. Farmers and GEICO did not offer telematics at all.

The study revealed some key industry findings. None of the insurers in the study offered UBI proactively. And in general, associates across channels were unprepared to speak to the telematics opportunity in depth. When it was discussed, price was the only incentive referenced as a reason to adopt telematics. Yet external research shows that some consumers would be interested in the program based on other benefits.

Also of note, UBI information is not offered consistently across channels, even when prompted by the customer. For example, the web is underutilized as a means of driving telematics adoption. This opens up an opportunity to empower every channel to execute on the strategy, and make sure the customer journeys are integrated.

Based on the findings, we recommend a few areas of focus to close the gaps in telematics adoption:

• Make telematics adoption a strategic priority across the enterprise.

• Set performance goals and measure telematics adoption.

• Proactively offer UBI in the channels that consumers prefer.

• Launch word of mouth, social media, and customer testimonials to increase UBI adoption.